Digital Oilfield Market The digital oilfield market consists of solutions and services that use data analytics and automation technology to optimize oil and gas exploration and production processes. Digital oilfield solutions integrate various information systems and software to help maintain safe operations, increase production efficiency, and maximize asset utilization. Digital technologies allow operators to remotely monitor field operations and optimize production processes in real-time.

The global Digital Oilfield Market is estimated to be valued at US$ 26.31 Bn in 2023 and is expected to exhibit a CAGR of 9.9% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: Optimizing production processes through digital oilfield solutions provides major growth opportunities for the market. Digital solutions help optimize drilling, reservoir management, and production processes to increase oil recovery rates. They allow producers to track assets remotely, automate workflows, and make data-driven decisions. This improves efficiency, avoids unplanned downtime, and maximizes profits over the lifecycle of oilfields. Optimizing production processes using digital technologies can significantly boost productivity and unlock untapped reserves, thereby driving the digital oilfield market during the forecast period. Porter's Analysis Threat of new entrants: The digital oilfield market requires high capital investments in advanced technologies which acts as a deterrent for new companies. Bargaining power of buyers: Large oil companies have significant bargaining power as buyers due to their strong financial standing and size of their operations forcing companies to compete intensely on pricing and services. Bargaining power of suppliers: Major technology providers have control over pricing and product design which gives them higher bargaining power in the market. Threat of new substitutes: Limited threat of substitutes as digital oilfield solutions have become integral part of upstream and midstream operations. Competitive rivalry: Intense competition exists among existing players to gain higher market share through continuous innovations and providing customized solutions. SWOT Analysis Strength: Digital oilfield solutions provide improved production efficiency, minimize non-productive time and reduce operating costs. Weakness: Requirement of high initial investments and skilled workforce for implementing advanced technologies poses challenges. Opportunity: Growing global energy demand and shift towards smart fields present significant growth opportunities. Threats: Volatile crude oil prices and economic slowdowns impact capital expenditure of oil companies. Key Takeaways The global Digital Oilfield Market Share is expected to witness high growth over the forecast period. North America currently dominates the market due large number of aging oilfields and focus on enhancing production. Europe is also a major region supported by increasing shale gas extraction activities. Asia Pacific is expected to grow at fastest pace led by China and India focusing on upgrading aging infrastructure. Key players operating in the Digital Oilfield Market are Sotrafa, Berry Global, NETAFIM, Certhon, Richel Group SA, Stuppy Greenhouse, Logiqs B.V., Argus Control Systems Ltd., Poly-Tex, Inc. Major players are investing in development of smart digital solutions for optimizing upstream and midstream operations. Intelligent wells concept and application of Internet of things is gaining popularity. Implementation of cloud computing and big data analytics is also growing across regions. Explore more related article on this topic: https://www.ukwebwire.com/digital-oilfield-market-is-expected-to-be-flourished-by-growing-adoption/

0 Comments

Polyunsaturated Fatty Acids Market is Polyunsaturated fatty acids (PUFAs) are fatty acids that help lower cholesterol levels and reduce the risk of heart diseases. They provide various health benefits such as improving heart health, brain function, skin, and joint health. Owing to the growing awareness about health benefits of PUFAs, the demand for PUFA-rich foods and supplements has significantly increased in recent years.

The global Polyunsaturated Fatty Acids Market is estimated to be valued at US$ 6.36 Bn in 2023 and is expected to exhibit a CAGR of 11% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: Reduced Risk of Heart Diseases The opportunity for growth in the polyunsaturated fatty acids market lies in the reduced risk of heart diseases. PUFAs such as omega-3 and omega-6 fatty acids play a vital role in maintaining heart health when consumed in recommended amounts. They help reduce triglyceride and LDL cholesterol levels, regulate heart rate and rhythm, and decrease inflammation. According to American Heart Association, diets rich in omega-3 fatty acids can reduce the risk of sudden death from cardiac arrest by around 45%. Owing to increasing awareness about this heart health benefit of PUFAs, their demand from pharmaceutical and nutraceutical industries for producing supplements is growing substantially. This is expected to contribute significantly to the market growth over the forecast period. Porter’s Analysis Threat of new entrants: The threat of new entrants in the polyunsaturated fatty acids market is moderate. Production of polyunsaturated fatty acids requires advanced technology and large capital investments which act as entry barriers for new players. However, some small players can enter by offering value added products or services. Bargaining power of buyers: The bargaining power of buyers in the polyunsaturated fatty acids market is high. Buyers have multiple suppliers to choose from so they can negotiate on price and quality. Substitute products also increase buyers bargaining power. Bargaining power of suppliers: The bargaining power of suppliers is moderate. Suppliers of raw materials like fish/flax oil have some control over pricing but major players in the market can also influence prices. Dependence on specific raw material suppliers is also less. Threat of new substitutes: Threat from substitute products is moderate to high. Products like monounsaturated fatty acids and saturated fatty acids are substitutes. Innovation in substitute products poses medium threat. Competitive rivalry: Competition in the market is high because of presence of many international and domestic players. SWOT Analysis Strength: Growing health awareness, ease of availability, wide range of end uses. Increasing use in nutraceuticals, infant formula and dietary supplements. Weakness: High R&D costs, vulnerability to supply chain disruptions. Price fluctuations of raw materials. Opportunity: Growing demand for plant-based and organic products. Innovations in application areas like personal care and animal feed. Threats: Stringent regulations regarding quality and production processes. Threat from substitute vegetable oils. Key Takeaways The global Polyunsaturated Fatty Acids Market Growth is expected to witness high growth due to increasing health consciousness. The Asia Pacific region currently dominates the global market and is expected to grow at the fastest rate during the forecast period. Rising incomes and growing awareness about health benefits of PUFAs are fueling market growth in the region. The global polyunsaturated fatty acids market is estimated to be valued at US$ 6.36 Bn in 2023 and is expected to exhibit a CAGR of 11% over the forecast period 2023 to 2030. Key players operating in the polyunsaturated fatty acids market are Advanced Organic Materials, Ariba, Inc. (SAP SE), Coupa Software Inc, GEP, Procurify, Sage Intacct, Inc. (The Sage Group PLC), Sievo, SutiSoft, Inc., TOUCHSTONE GROUP PLC, VA Tech Ventures Pvt Limited (Happay), and others. The industry is driven by strategic initiatives like acquisitions, expansions and new product launches by major manufacturers. Advanced Organic Materials and Ariba, Inc. (SAP SE) are market leaders in terms of sales and operational footprint. Explore more related article on this topic: https://www.ukwebwire.com/polyunsaturated-fatty-acids-market-poised-for-growth/  Polysilicon Market Polysilicon or polycrystalline silicon is a high-purity silicone material used as raw material in the production of photovoltaic cells used in solar panels. It has high light absorption capacity and is a more efficient alternative to conventional materials used in photovoltaic cells. The growing demand for solar energy and government support for renewable energy sources is driving the growth of the polysilicon market. With increasing focus on controlling carbon emissions, more countries are setting renewable energy targets and investing in solar energy infrastructure development. This is expected to boost the demand for solar panels and subsequently polysilicon as a core component.

The global Polysilicon Market is estimated to be valued at US$ 12.8 Bn in 2023 and is expected to exhibit a CAGR of 6.3% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: The surging demand from the renewable energy sector presents a key growth opportunity for the polysilicon market. Solar energy has emerged as one of the most viable and affordable renewable energy sources and global solar capacity addition has been growing at a strong pace over the past few years. According to the International Energy Agency (IEA), global solar PV capacity is expected to grow at an average annual rate of 17% through 2026. This rising focus on solar energy to meet renewable targets along with achieving carbon neutrality goals will drive up the demand for polysilicon as a key material in solar photovoltaic panels. The market players can leverage this opportunity by expanding their production capacities and capabilities to meet the growing polysilicon needs of the solar industry. Strategic partnerships with solar panel manufacturers would help secure long term demand. Porter's Analysis Threat of new entrants: The polysilicon market requires massive capital investments for setting up production facilities and technology to produce polysilicon. This poses significant entry barriers for new players. Bargaining power of buyers: The presence of multiple established players in the polysilicon market gives buyers considerable bargaining power to negotiate on pricing and other terms. Bargaining power of suppliers: A few major players dominate the raw material supply chain for polysilicon production giving them strong influence over pricing. Threat of new substitutes: At present, there are no direct substitutes for polysilicon. Advancements in thin-film photovoltaic technologies pose a potential threat. Competitive rivalry: The polysilicon market is highly competitive with major players competing on cost leadership, product quality and technical capabilities. SWOT Analysis Strengths: Rising solar installations worldwide and government support for clean energy boost demand. Weaknesses: High capital requirements and fluctuations in silicon prices impact profits. Supply chain disruptions affect production. Opportunities: Increasing uptake of heterojunction solar PV technology presents an opportunity. Growing solar rooftop markets in developing nations offer scope. Threats: Trade restrictions and tariff policies impact supply and costs. Climate change policies influence long term demand prospects. Key Takeaways The global Polysilicon Market Demand is expected to witness high growth over the forecast period of 2023 to 2030. Rapid capacity additions in solar PV manufacturing mainly in China and increasing policy support for renewable energy in European and Asian countries will drive the demand for polysilicon. Regionally, Asia Pacific dominates the polysilicon market currently and is projected to continue its lead, supported by China's massive production and installation base for solar PV. Key players operating in the polysilicon market include GCL-Poly Energy Holdings, Wacker Chemie, OCI, Hanwha Solutions, Tokuyama Corporation, DAQO New Energy, Mitsubishi Materials Corporation. These players are focusing on ramping up production capacities to meet the rising global demand. Tier 2 players are expanding through partnerships for technology access and to gain access to global markets. Explore more related article on this topic: https://www.ukwebwire.com/polysilicon-market-is-expected-to-be-flourished-by-growing-demand/  Polyolefin Resins Market Polyolefin resins are a category of polymers produced from olefin monomers such as ethylene and propylene through polymerization process. Polyolefin resins have excellent physical and mechanical properties such as high tensile strength, chemical resistance and durability making them suitable for wide range of applications in packaging, automotive, medical devices and construction industries.

The global Polyolefin Resins Market is estimated to be valued at US$ 255.82 Bn in 2023 and is expected to exhibit a CAGR of 8.1% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: The opportunity in infrastructure development is expected to propel the growth of the Polyolefin Resins Market. Rapid urbanization and industrialization in developing economies has increased the need for infrastructure development including roads, bridges, rail, buildings etc. Polyolefin resins find extensive applications in construction due to their versatility and durability. They are used in manufacturing cables, pipes, geomembranes, sheetings and others. The ongoing projects of highways, metros, smart cities and other public infrastructure in countries across Asia Pacific and Latin America will demand significant amount of polyolefin resins over the forecast period. The growing infrastructure development is likely to open new avenues for polyolefin resin manufactures. Porter’s Analysis Threat of new entrants: The polyolefin resins market requires high capital investments, which acts as a major barrier for new players. Stringent regulations related to product quality and safety further increases the entry barriers. Bargaining power of buyers: Buyers have moderate to high bargaining power due to availability of substitute products and undifferentiated nature of products. Bargaining power of suppliers: The suppliers have low to moderate bargaining power due to availability of numerous suppliers in the market. Threat of new substitutes: Threat of substitutes is moderate due to presence of alternative products like PVC, ABS, nylon etc. along with difficulty in product substitution due to high switching costs. Competitive rivalry: The market is highly competitive due to presence of numerous global and regional players. SWOT Analysis Strength: High growth driven by increasing applications in packaging, construction and automotive industries. Polyolefins are cost effective and have high strength to weight ratio. Weakness: Volatility in raw material prices lead to fluctuating product costs. Vulnerable to economic slowdowns impacting end use industries. Opportunity: Rising demand from emerging economies of Asia Pacific and Central & South America. Ongoing product innovations resulting in development of new grades. Threats: Stringent regulations due to environmental concerns over non-biodegradability. Threat from substitutes expanding product portfolio. Key Takeaways The global Polyolefin Resins Market Demand is expected to witness high growth during the forecast period of 2023-2030. The global Polyolefin Resins Market is estimated to be valued at US$ 255.82 Bn in 2023 and is expected to exhibit a CAGR of 8.1% over the forecast period 2023 to 2030. The Asia Pacific region dominated the market in 2024 with China being the largest producer and consumer. Key players operating in the polyolefin resins market are Accruent, Archibus, FM:Systems Group, LLC, IBM TRIRIGA, iOFFICE, OfficeSpace Software, Planon, QuickFMS, and SPACEWELL INTERNATIONAL. The demand is driven by packaging industry followed by construction and automotive sectors. Polyethylene and polypropylene are major product types with linear low density polyethylene (LLDPE) resin capturing largest share. Ongoing developments in resin properties and product innovation are helping polyolefins find new applications. Strict regulations on emissions and disposal due to non-biodegradability present challenges for market growth. Check below related articles on this topic: https://www.newsanalyticspro.com/polyolefin-resins-market-is-expected-to-flourish-by-growing-demand/  Polymer Emulsion Market Polymer emulsions are water-based dispersions of finely divided polymer particles stabilized by surfactants. They are extensively used in numerous applications such as paints & coatings, paper & paperboards, textiles & fibers, and adhesives & sealants. These emulsions provide benefits such as easy application, non-toxicity, and low volatile organic compound emissions. The growing construction activities as well as increasing focus on environment-friendly products are fueling the demand for polymer emulsions across the globe.

The global Polymer Emulsion Market is estimated to be valued at US$ 33.18 Bn in 2023 and is expected to exhibit a CAGR of 16% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: Increasing demand from various end-use industries is estimated to offer lucrative growth opportunities for polymer emulsion market. The paints & coatings sector is the largest consumer of polymer emulsions due to their extensive use in architectural and industrial coatings. Additionally, environmental regulations banning the use of solvent-based adhesives are promoting the adoption of water-based polymer emulsion adhesives in various end-use industries like packaging, construction, woodworking, and automotive. Moreover, the rising demand for paper from food packaging and tissue industries is augmenting the consumption of polymer emulsions in paper processing. Thus, the growing requirements from diverse applications across industries are expected to boost the demand for polymer emulsions during the forecast period. Porter's Analysis Threat of new entrants: The threat of new entrants is low because manufacturing polymer emulsions requires high capital investment and technical expertise. Established players enjoy economies of scale in production and distribution. Bargaining power of buyers: The bargaining power of buyers is moderate. Buyers have several suppliers to choose from for polymer emulsions. However, switching costs are low. Bargaining power of suppliers: The bargaining power of suppliers is low due to availability of substitutes and limited differentiation in raw materials. Suppliers do not have pricing power. Threat of new substitutes: The threat of substitutes is moderate. Some substitutes include solvent-borne polymers and water-borne polymer dispersions. However, polymer emulsions are environment-friendly. Competitive rivalry: Competition in the polymer emulsion market is high due to presence of numerous international and regional players. Players compete based on product quality, price, and innovation. SWOT Analysis Strengths: Polymer emulsions offer several advantages over organic solvents such as being non-toxic, non-flammable and environment-friendly. Wide applications in industries like paints & coatings. Weaknesses: Issues with emulsion stability and higher production costs. Vulnerable to fluctuations in raw material prices. Opportunities: Growing end-use industries like construction and automotive present new avenues. Potential in emerging economies of Asia Pacific and Latin America. Threats: Stringent environmental regulations around the globe increase compliance costs. Threat from substitutes limits pricing flexibility. Key Takeaways The global Polymer Emulsion Market Demand is expected to witness high growth during the forecast period due to increasing use of Polymer Emulsion in paints & coatings industry. The global polymer emulsion market is estimated to be valued at US$ 33.18 Bn in 2023 and is expected to exhibit a CAGR of 16% over the forecast period 2023 to 2030. The Asia Pacific region dominates the global market and is expected to grow at a high rate due to rising construction and industrial activities in China, India. Growth in the construction and automotive industries drives demand. Key players: Key players operating in the Polymer Emulsion market are VIVUS Inc., Pfizer Inc., Novo Nordisk, Bayer AG, F Hoffmann-La Roche, Glaxosmithkline, Arena Pharmaceuticals, Eisai Co. Ltd., Takeda Pharmaceutical Company, and Nalpropion Pharmaceuticals Inc. Explore more related article on this topic: https://www.ukwebwire.com/polymer-emulsion-market-is-expected-to-be-flourished-by-increasing-demand/ Hydrogen Buses Market Is Estimated To Witness High Growth Owing To Opportunity In Reducing Emissions1/2/2024  Hydrogen Buses Market Hydrogen buses are zero-emission buses that use hydrogen as fuel through fuel cell technology to power their electric motors. They do not produce any emissions and only emit water vapor and warm air. With rising environmental concerns, many cities and transit agencies are turning to zero-emission hydrogen buses as an alternative to diesel buses. Hydrogen buses provide longer range than electric buses powered by batteries and can be refueled faster than recharging electric buses.

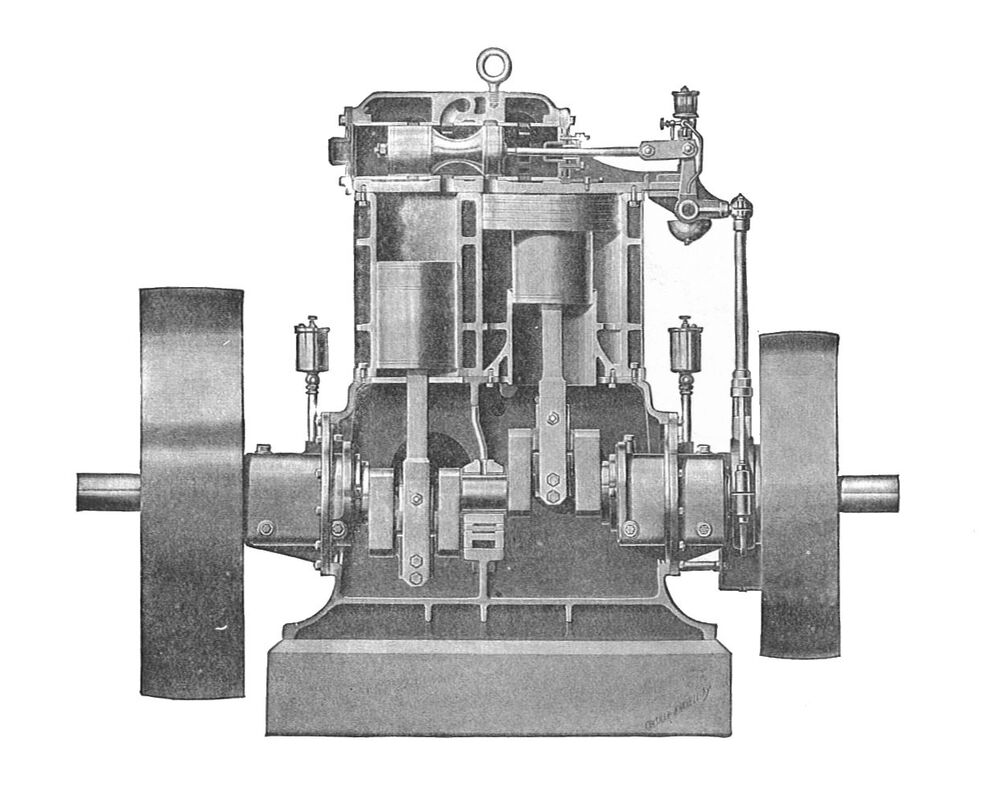

The global Hydrogen Buses Market is estimated to be valued at US$ 10.78 billion in 2023 and is expected to exhibit a CAGR of 14% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: The opportunity in reducing emissions through use of hydrogen buses presents significant growth prospects for the hydrogen buses market. Stringent emission standards by regulatory bodies worldwide are compelling transit agencies and municipal corporations to adopt clean fuel technologies. Hydrogen buses produce no tailpipe emissions and are increasingly being recognized as a viable technology to reduce air pollution in urban areas. Many cities have initiated pilot projects and placed orders for hydrogen buses to evaluate their performance under local operating conditions. Further policy support in the form of subsidies and favorable incentive schemes for hydrogen infrastructure development can boost the adoption of hydrogen buses and drive the market growth over the forecast period. Porter’s Analysis Threat of new entrants: Low capital requirements and the availability of used buses limit the threat of new entrants. However, established manufacturers have scale advantages and strong relationships with transit agencies that make entry difficult. Bargaining power of buyers: Large transit agencies have significant bargaining power as they can influence bus manufacturers and negotiate low prices for bulk orders. However, switching costs when transitioning bus fleets limits this power. Bargaining power of suppliers: A few large integrated manufacturers supply hydrogen fuel cells and storage systems globally. This concentrates supplier power, especially due to high development costs. Regional manufacturers may face higher costs and less bargaining power. Threat of new substitutes: Battery electric buses continue advancing and may substitute hydrogen buses for shorter-range applications. However, hydrogen has advantages for large fleets needing extended range. Competitive rivalry: Manufacturers compete based on fuel efficiency, reliability and total cost of ownership. Rivalry is intense as bus makers vie for large contracts from cities transitioning to low and zero-emission buses. SWOT Analysis Strengths: Hydrogen has a higher energy density than batteries, enabling extended range. Proven technology with declining fuel cell and storage costs. Zero tailpipe emissions support environmental targets. Weaknesses: High capital cost of buses, lack of hydrogen refueling infrastructure in most cities. Complex fuel storage presents safety and maintenance challenges. Public perception lags battery electric buses. Opportunities: Strategic government support and initiatives drive heavy investment in hydrogen economy. Fuel cell integration into other transport modes increases adoption. Global collaboration to establish fueling networks expands addressable markets. Threats: Battery technology continues advancing rapidly, potentially surpassing hydrogen buses for shorter routes. Lack of coordination between stakeholders delays infrastructure build-out. Supply chain disruptions impact production costs and timelines. Key Takeaways The global Hydrogen Buses Market Demand is expected to witness high growth over the forecast period supported by strategic government initiatives and environmental regulations. Regional analysis: Europe and North America are also expanding their hydrogen bus fleets. Countries like Germany, France and UK in Europe and US and Canada in North America offer strong policy and financial support to develop hydrogen ecosystems including buses. Over 400 hydrogen buses were ordered in Europe by 2022 to be deployed across various cities. Key players operating in the hydrogen buses market are LG Chemicals Ltd. (South Korea), Cabot Corporation (US), Jiangsu Cnano Technology Co., Ltd. (China), Resonac Corporation (Showa Denko K.K.) (Japan), and Arkema S.A. (France). These players are focusing on improving fuel cell performance and efficiency while reducing costs. Get More Insights On This Topic: https://www.newsanalyticspro.com/hydrogen-buses-market-demand-share-analysis/  High Speed Engine Market High-speed engines are engines capable of operating at speeds greater than 2,500 rpm. They are used in diverse applications such as automobiles, aircraft, motorcycles, watercraft, and others. High-speed engines offer benefits such as improved fuel efficiency, reduced carbon emissions, increased power output, and better drivability compared to conventional engines. The growing demand for high-performance vehicles from automotive and transportation industries is propelling the demand for high-speed engines.

The global High Speed Engine Market is estimated to be valued at US$ 19.83 Bn in 2023 and is expected to exhibit a CAGR of 4.3% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: The growing transportation industry across the globe presents lucrative growth opportunities for the high speed engine market. Rapid urbanization and rising incomes are augmenting passenger travel, prompting increased investment in public transportation infrastructure. Further, international trade and tourism activities are witnessing strong growth. This is increasing demand for aircraft, ships, locomotives, and automobiles equipped with efficient and powerful engines. Manufacturers can focus on developing innovative high speed engines catering to the specific needs of diverse transportation sectors to leverage the extensive opportunities in this industry. Porter’s Analysis Threat of new entrants: High speed engine market require sizable R&D investments and capabilities to develop high-end technologies. Established players enjoy economies of scale. Bargaining power of buyers: Buyers have moderate bargaining power due to availability of substitutes. However, differentiated needs of end-users provide some customer lock-in. Bargaining power of suppliers: Few technology providers enjoy strong bargaining power due to proprietary process know-how and IP. Suppliers integrate vertically to control costs and ensure quality. Threat of new substitutes: Emerging powertrain technologies pose threats, but high-speed engines have advantages in applications requiring high power density and torque. Competitive rivalry: Intense competition among major players to gain larger market share through continuous technological upgrades and expanded product portfolios. SWOT Analysis Strength: Differentiated technologies, manufacturing expertise, global distribution network and customer base. Weaknesses: High R&D costs, pricing pressures from low-cost players, dependence on few platform technologies. Opportunities: Growth in aerospace, marine and off-highway vehicle segments. Adoption in hybrid-electric systems offers new avenues. Threats: Declining global demand amid economic uncertainties. Stringent emission norms shift focus to alternative powertrains. Key Takeaways The global High Speed Engine Market Share is expected to witness high growth over the forecast period aided by recovery in end-use industries post-pandemic. Regional analysis: North America currently dominates owing to strong aerospace and defense manufacturing base in the region. However, Asia Pacific is expected to be the fastest growing market led by China, India and Southeast Asian countries. Key players operating in the high speed engine market are Panasonic Corporation, Energizer Holdings, Maxwell Technologies Inc., Seiko Instruments Inc., Berkshire Hathaway Inc., Sony Corporation, Toshiba Corporation, Renata SA, Camelion Battery, and Varta AG. The market is consolidated in nature with major players focusing on product development and partnerships to cater diverse application segments. Get More Insights On This Topic: https://www.ukwebwire.com/high-speed-engine-market-demand-analysis/  High Performance Doors Market High performance doors are industrial grade doors primarily used in commercial spaces, industrial and logistics facilities. These doors are engineered to withstand harsh weather conditions, provide high insulation value and strengthen overall security of facilities. High performance doors offer low maintenance, easy operation, energy efficiency and enhance productivity. The rising focus on automation of facilities for optimized operations is driving demand for these automated doors.

The global High Performance Doors Market is estimated to be valued at US$ 4.28 Bn in 2023 and is expected to exhibit a CAGR of 5.9% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Dynamics: Increasing Demand in Industrial Sector: High performance doors are widely used across various industrial verticals such as warehouses, logistics facilities, commercial spaces and manufacturing plants. Rapid industrialization and growth of e-commerce sector has augmented demand for efficient and automated industrial doors in developing and developed nations. Moreover, focus on automation of facilities is empowering deployment of high performance doors for optimized operations. Growing Demand for Energy Efficient Doors: High performance doors provide superior insulation against temperature, sound and dust compared to conventional doors. They minimize heat transfers and optimize energy usage of facilities. Stringent regulations regarding energy consumption across countries is propelling the replacement of conventional doors with energy efficient high performance doors. This is a major factor accounting for market growth over the forecast period. SWOT Analysis Strength: High performance doors have high energy efficiency which results in lower operating costs for end-users. They offer fast operation for high traffic areas which improves productivity. These doors also have tight seals that help maintain optimum internal environment conditions. Weakness: High performance doors have high initial installation and maintenance costs compared to conventional doors. Their complex designs require specialized expertise for installation and repairs. Opportunity: Growing focus on green buildings and sustainable construction practices is driving the demand for energy efficient doors. Rapid urbanization in developing nations is also increasing the need for space optimization solutions in commercial buildings. Threats: Availability of cheap alternatives may limit the demand growth. Economic slowdowns can negatively impact the commercial real estate sector and hamper market revenues. Supply chain disruptions due to Covid-19 pandemic are also posing short term challenges. Key Takeaways The global High Performance Doors Market Size is expected to witness high growth over the forecast period owing to increasing focus on energy efficiency and sustainability in the construction industry. Rapid urbanization and growth of green buildings are major drivers facilitating the demand for these doors across regions. Regional analysis: North America currently dominates the market with largest revenue share. However, Asia Pacific is projected to offer lucrative opportunities backed by strong growth of the building construction sector in China and India. These nations are also implementing various construction standards and regulations to promote sustainable infrastructure development. Key players: Key players operating in the high performance doors market are Koninklijke Philips N.V., LifeWatch USA, Tunstall, Apple Inc., ADT Security Services, Medical Guardian LLC, MobileHelp, Bay Alarm Company, MariCare Oy, Origin Wireless, The ADT Corporation, Singapore Technologies Electronics Limited, Semtech Corporation. They are focusing on launching innovative and customized door solutions to expand their geographic footprint. Get More Insights On This Topic: https://www.ukwebwire.com/high-performance-doors-propelled-by-enhanced-energy-efficiency/  Heat Exchanger Market Heat exchangers are devices designed and constructed to transfer heat from one medium to another with minimum temperature difference. They are used in a wide range of industries including HVAC, power generation, chemical, petrochemical and oil & gas. Heat exchangers offer high efficiency and reliability while transferring heat between fluids without direct contact. They play a vital role in heavy industries by transferring heat from steam, process liquids and gases.

The global Heat Exchanger Market is estimated to be valued at US$ 18849.18 Mn in 2023 and is expected to exhibit a CAGR of 1.2% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: The increasing focus on nuclear power generation across the globe provides lucrative opportunity for growth of the heat exchanger market. Nuclear power plants use numerous heat exchangers for steam generation, power conversion, cooling and other ancillary systems. Heat exchangers act as crucial components for efficient energy production through nuclear fission. They transfer heat from radioactive coolants without risk of leakage or contamination. With growing emphasis on reducing carbon emissions, many countries are expanding their nuclear power capacities. This is expected to drive significant demand for specialized heat exchangers optimized for nuclear applications. The development of advanced nuclear technologies also offers new opportunities. Sustained investments in reactor safety and lifetime extension of existing plants will further augment the nuclear heat exchanger market in the coming years. Porter’s Analysis Threat of new entrants: Explain in the heat exchanger market, the threat of new entrants is medium as it requires high capital investment in R&D, technology and manufacturing facilities. Bargaining power of buyers: Buyers have medium bargaining power in this market as heat exchangers are essential equipment and there are multiple global players. Bargaining power of suppliers: Suppliers have low to medium bargaining power as raw materials required are widely available and there are substitute materials also available. Threat of new substitutes: Threat of new substitutes is low as heat exchangers have well established applications and substitution would require change in plant design. Competitive rivalry: The competitive rivalry is high as the market is fragmented with presence of many global and regional players. SWOT Analysis Strengths: Heat exchangers offer enhanced process efficiency and cost savings. Manufacturers have strong R&D capabilities to develop innovative products. Weaknesses: Initial investments required are high. Require skilled workforce for complex manufacturing processes. Opportunities: Growing demand from petrochemicals, power plants, HVAC industry. Increasing applications in renewable energy sector. Threats: Trade barriers and regulations. Short product life cycles require continual innovations. Key Takeaways The global Heat Exchanger Market Growth is expected to witness high growth on account of rising energy demand worldwide. The global heat exchanger market is estimated to be valued at US$ 18849.18 Mn in 2023 and is expected to exhibit a CAGR of 1.2% over the forecast period 2023 to 2030. Regional analysis - Asia Pacific dominates the global heat exchanger market with a share of over 35% in 2023. China, India being major consumers due to rapid industrialization. Key players - Key players operating in the heat exchanger market are GE-Hitachi Nuclear Energy Inc., Westinghouse Electric Company LLC, STP Nuclear Operating Company, SKODA JS AS, China National Nuclear Corporation, Bilfinger SE, BWX Technologies Inc., Doosan Heavy Industries & Construction Co. Ltd, Mitsubishi Heavy Industries Ltd, Bechtel Group Inc., Japan Atomic Power Co., and Rosatom Corp. Innovation and development of advanced materials for heat exchangers will remain key focus areas. Adoption of energy efficient products present new opportunities. Stringent regulations may impact revenues of certainplayer. Get More Insights On This Topic: https://www.ukwebwire.com/the-global-heat-exchanger-market-demand-share-analysis/  Headlight Control Module Market Headlight control modules are electronic devices that are installed in vehicles to control and regulate the lighting functions of headlights, fog lamps, and daytime running lights. Headlight control modules enhance driver convenience and safety by automatically adjusting the headlight beam intensity based on ambient light conditions. They help improve visibility for drivers during nighttime and low-light conditions. The growing automotive industry and strict regulations regarding vehicle safety are fueling the demand for advanced automotive lighting systems with enhanced features.

The global Headlight Control Module Market is estimated to be valued at US$ 4.58 Bn in 2023 and is expected to exhibit a CAGR of 15.% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Opportunity Rising Demand for Autonomous Vehicles: The development of autonomous vehicles is creating new opportunities for headlight control modules. Advanced headlight control systems play a vital role in ensuring safety in autonomous driving conditions by automatically adjusting headlight functions based on diverse driving situations. The growing R&D towards developing self-driving cars will significantly drive the demand for intelligent and adaptive headlight control modules in the coming years. Porter's Analysis Threat of new entrants: The threat of new entrants in the headlight control module market is moderate. The sizable R&D investment required for product development and the need for robust supply chain pose a barrier for new players to enter the market. However, availability of innovative technology and growing demand for advanced automotive lighting solutions provides opportunities for new entrants. Bargaining power of buyers: The bargaining power of buyers in the headlight control module market is high. The presence of several established automakers gives buyers the leverage to negotiate on price and demand value-added features. Buyers can also switch between suppliers based on cost and performance. Bargaining power of suppliers: The bargaining power of suppliers is moderate. While a few large players dominate the supply of key components such as LEDs and sensors, availability of substitute materials and scope for backward integration exercises control over suppliers' bargaining ability. Threat of new substitutes: Threat of substitutes is low as headlight control modules have no close substitute. Emerging lighting technologies can disrupt the market but are still in development stages and are not viewed as direct substitutes. Competitive rivalry: The competitive rivalry is high owing to presence of numerous global and regional players offering customized solutions. Players compete based on technology, quality, reliability, pricing and innovation to gain market share. SWOT Analysis Strengths: Growing demand for enhanced safety features and stringent regulations regarding vehicle lighting are driving market growth. Continuous technological advancements offer improved performance. Weaknesses: High R&D costs and design complexities associated with the modules increase the price of vehicles. Occasional technical glitches can cause recalls. Opportunities: Connected vehicles and autonomous driving present new areas of application. Emergence of LiDAR and laser technologies will change automotive lighting landscape in long run. Threats: Economic slowdowns can impact automobile sales and subsequently module demand. Dependence on semiconductor supply makes the industry vulnerable to disruptions. Trade conflicts and geopolitical issues exert pricing pressure. Key Takeaways The global Headlight Control Module Market Share is expected to witness high growth over the forecast period of 2023 to 2030. Regional Analysis: Asia Pacific currently dominates the market with China, Japan and India being the major markets. The region is expected to maintain its lead backed by increasing vehicle production and rising disposable incomes. Key players operating in the headlight control module market are Phantom Buster, Mozenda, Inc., Hangzhou Duosuan Technology, SysNucleus, Octopus Data Inc., Newprosoft, and more. Regional analysis related content comprises increased focus of automakers on upgrading lighting technology and compliance with stringent safety regulations in the region provide opportunities for headlight control module market players to penetrateAsia Pacific market further. Get More Insights On This Topic: https://www.pressreleasebulletin.com/headlight-control-module-market-demand-analysis/ |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

November 2023

Categories |

RSS Feed

RSS Feed